Retirement tax planning is not just about what you pay this year. It is about shaping the future of your plan before your options narrow.

A Roth conversion before retirement can sometimes create more tax flexibility later, especially if widowhood, required minimum distributions (RMDs), or Medicare premiums may affect your long-term plan.

Most people think about retirement in terms of investments, income, and whether they will have enough to live the lifestyle they want. Those questions matter. But taxes matter too. In some cases, they matter more than people realize.

That is especially true in the years leading up to and just after retirement, when there may be a meaningful opportunity to decide whether a Roth conversion makes sense.

A Roth conversion, at its most basic level, means moving money from a traditional IRA or other pre-tax retirement account into a Roth IRA and paying tax on the converted amount now. In return, you may reduce future pre-tax balances, lower future required minimum distributions, and create more flexibility later, because Roth IRAs are not subject to lifetime RMDs for the original owner.

A Roth conversion is not inherently good or bad. It is a trade-off. In some households, it can improve long-term flexibility. In others, it can create a tax bill, trigger higher Medicare premiums, reduce Affordable Care Act (ACA) Marketplace premium assistance, or push income into a less favorable range without providing enough long-term benefit to justify the cost.

But the real question is not whether Roth conversions are good or bad.

The real question is this: Does paying some tax now improve the overall shape of your financial plan?

For many women, that question deserves even more attention. Retirement planning is not only about income. It is also about resilience. It is about preparing for life transitions before they happen. One of the most important, and most overlooked, of those transitions is widowhood.

For many women, this matters even more because women often live longer than men, which can mean more years of managing taxes, distributions, healthcare costs, and investment decisions on their own.

Quick Takeaways

- A Roth conversion before retirement may be worth evaluating when future RMDs, widowhood, or Medicare premiums could create a worse tax picture later.

- The goal is not to minimize this year’s taxes. It is to improve long-term flexibility.

- The right answer depends on the full plan, including brackets, IRMAA, ACA costs, cash available to pay the tax, and legacy goals.

Why Timing Matters for a Roth Conversion Before Retirement

For many households, the best time to evaluate a Roth conversion is not after the time to start RMDs has already arrived. It is earlier.

There is often a stretch of years after work when income declines, before Social Security and RMDs fill up your tax return and fill your most favorable tax brackets. That window can create room to make thoughtful tax decisions while you still have options. Once RMDs begin, they create mandatory taxable income each year, while Roth IRAs generally do not create lifetime RMDs for the original owner.

That does not mean everyone should rush to convert.

It does mean that the years before RMDs begin may offer more planning flexibility than the years after they begin.

A Real Example of Why Timing Matters

The examples below are simplified, anonymized illustrations. Actual Roth conversion decisions depend on income sources, deductions, filing status, account mix, time horizon, and the ability to pay the tax from other assets.

I have seen this play out in real life.

A couple retires and begins doing annual Roth conversions, carefully filling a specific tax bracket without crossing into the next one. In one case that comes to mind, the bracket we targeted was the 12% bracket. Going further would have meant moving into the 22% bracket, so the goal was not to convert everything possible. The goal was to convert thoughtfully, year by year, while the tax cost was still relatively attractive.

Then one spouse died.

In the year of death, I told the surviving spouse that this would likely be the last year we could complete Roth conversions while staying in the 12% bracket. Once we looked ahead at the survivor’s Social Security benefit, required minimum distributions, and pension income, it became clear that as a single filer, that income alone would likely place her in the 22% bracket.

That is the kind of shift many people do not fully see coming.

Nothing about her life had suddenly become extravagant. Nothing about her spending had exploded. But her filing status changed. Her tax brackets changed. Her planning options narrowed.

That is why I do not think Roth conversions should be framed only as a tactic. They are part of a larger planning question. Does it make sense to pay some tax now, while you still have room, to reduce the risk of paying more tax later when the surviving spouse has fewer good options?

In this case, the couple was already a few years into retirement when we began working together, so there had not been as many opportunities to act earlier. There was also resistance to incurring a marginal tax rate of 22% or higher. If planning had started sooner, the long-term tax picture might have been better.

That does not mean Roth conversions are always the answer. It does mean that timing matters, and that waiting can carry a cost too.

Why Widowhood Changes the Math

When one spouse dies, the surviving spouse often continues to receive the higher of the couple’s two Social Security benefits, pension income (if applicable), and required distributions from retirement accounts, but now files as a single taxpayer. In many cases, that means similar income is now taxed less favorably because it fits into narrower single-file brackets. That is one reason widowhood can create a meaningful tax squeeze.

In situations like this, Roth conversion planning may deserve especially careful review.

The issue is not only whether the couple can afford the tax on a conversion today. The issue is whether reducing future pre-tax balances now could help the surviving spouse later, when brackets are narrower, and flexibility may be more limited.

That is a different way to think about taxes.

It is not about minimizing tax on this year’s return at all costs. It is about looking ahead and asking whether some tax paid now could lower the tax burden, or improve flexibility, over the rest of the survivor’s life.

I have heard people say how happy they are when they owe almost nothing in taxes in a given year. That can sound appealing on the surface. But by itself, it does not necessarily mean the long-term plan is improving. In many cases, it is worth evaluating whether using lower tax brackets now could improve the long-term outcome, especially if failing to do so may leave the surviving spouse in a higher bracket later.

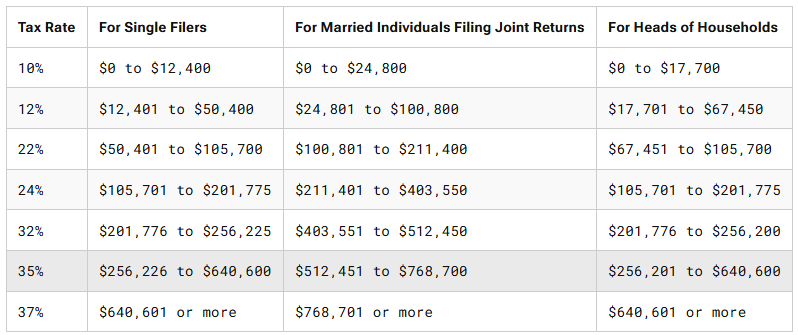

One reason this matters is that widowhood can sharply reduce the amount of income that falls into lower tax brackets. The chart below shows how much sooner a single filer can move into higher brackets than a married couple filing jointly. That does not mean everyone should automatically convert to the top of a bracket. It does mean the window for lower-rate Roth conversions can narrow meaningfully after the first spouse dies.

2026 Federal Income Tax Brackets: Single, Married Filing Jointly, and Head of Household

Source: Internal Revenue Service, “Revenue Procedure 2025-32”

That is why Roth conversion planning is often easier to do proactively than reactively.

IRMAA Matters Too

I have another couple I am working with who are currently in their 70s. I started working with them when they were already in their early 70s, and we have been doing Roth conversions since we started working together, at least partly because of the potential future consequences for the surviving spouse.

When we looked at conversions in 2025, one of the key points in our discussion was not just income tax. It was the Income Related Monthly Adjustment Amount (IRMAA). As your income surpasses certain income levels (for 2026, the first such level starts at $109,000 for single filers and $218,000 for couples filing jointly), your Medicare insurance premiums (Parts B and D) increase.

As a couple, we could evaluate how much conversion room they had while still staying within a level that made sense. But when we projected the surviving spouse’s likely future income, driven mainly by Social Security benefits and required minimum distributions, it became clear that the survivor would likely end up in at least the first IRMAA bracket as a single filer.

That matters because Medicare premiums are not based only on what is happening today. The Social Security Administration (SSA) says IRMAA is generally determined using the most recent federal tax return the IRS has on file, usually from two years earlier. In other words, higher income now can affect Medicare premiums later.

So in this case, the question was not simply, “Should we avoid conversions because they increase income?” The better question was, “Does it make sense to complete conversions now, at levels we can control, because doing so may help reduce future RMDs, future taxes, and future IRMAA exposure for the surviving spouse?”

In some cases, the answer may be yes. In others, the added tax cost or other trade-offs may outweigh the benefit.

That is another reason Roth conversion planning has to be evaluated over time, not just year by year. It is not only about the current tax return. It is about how today’s decisions may affect future tax brackets, future Medicare premiums, and the financial flexibility of the surviving spouse.

Current Tax Law Can Affect the Analysis

Recent tax law changes are not central to the strategy, but they are worth mentioning.

Current tax law can change how much room you have for a Roth conversion or how costly it is to recognize extra income in a given year. For example, the IRS says that for 2025 through 2028, eligible individuals age 65 and older may claim an additional $6,000 deduction, with phaseouts beginning above modified adjusted gross income (MAGI) of $75,000 for single filers and $150,000 for joint filers. For some retirees, that may create a little more room for thoughtful conversions.

There are also households for whom itemized deductions matter. In 2025, the state and local tax (SALT) deduction limit increased to $40,000 for single and married filers, with reductions above certain income levels, so for some higher-income households, that change can slightly affect the conversion math.

These are planning wrinkles, not the central story. But they serve as reminders to evaluate potential Roth conversions under the current law, not by what applied in the past.

ACA Premiums Can Change the Real Cost

There is another issue that warrants brief mention because it can materially affect the cost of a Roth conversion for some households.

If a client or family is receiving coverage through the ACA Marketplace, higher income from a Roth conversion can reduce premium tax credit eligibility and increase what they pay for health insurance. HealthCare.gov says income changes can affect the coverage or savings you are eligible for, and people who use more premium tax credit than they ultimately qualify for may have to reconcile and repay excess amounts when they file.

That is not a reason to avoid Roth conversions altogether. It is a reason to be careful.

For households on ACA Marketplace coverage, the true cost of a conversion is not always just the additional income tax. It may also include higher net health insurance premiums. That is especially relevant now because HealthCare.gov says the extra ACA Marketplace coverage savings tied to the pandemic-era expansion ended on December 31, 2025, and people who qualify for savings in 2026 will likely pay more for ACA Marketplace coverage than they did before.

So for some families, Roth conversion planning is not only about tax brackets and RMDs. It is also about healthcare costs.

Think in Lifetime Taxes, Not Just This Year’s Taxes

One of the biggest mistakes people make is evaluating Roth conversions only through the lens of this year’s tax return.

That is too narrow.

The real question is not, “Will this increase my taxes this year?” Of course, it might. That is often the point.

The better question is, “Could this reduce taxes over the rest of my life, or create more flexibility in the years when flexibility may matter most?”

Sometimes the answer is yes.

If future RMDs are likely to be large, if widowhood would push the surviving spouse into a less favorable tax picture more quickly, or if future income sources will leave little room for lower-bracket conversions later, then paying some tax now may improve the overall plan. IRS guidance confirms that traditional IRA balances drive future RMDs, while the original owner’s Roth IRA does not create a lifetime RMD requirement.

That is why I think Roth conversion planning is best viewed as a lifetime, not a one-year, tax decision.

Legacy Matters Too

There is another layer here that I do not think gets enough attention.

This planning is not only about the couple during retirement or the surviving spouse. It may also affect what happens after both spouses are gone.

If significant money remains in traditional IRAs and eventually passes to children, those dollars may carry a future tax burden for them as well. IRS guidance explains that beneficiaries of inherited retirement accounts remain subject to distribution rules after the account owner dies, and that inherited retirement accounts can generate taxable income for heirs depending on the type of account and the applicable rules.

That does not mean every family should prioritize legacy over present needs. It does mean that good Roth conversion planning can sometimes benefit more than one generation.

Many of the women I work with care deeply about helping their children, not only through what they leave behind but also through how thoughtfully they plan. When done well, Roth conversions may help support the widow, reduce future tax pressure, and leave a more flexible legacy for the next generation.

Many non-spouse beneficiaries who inherit Roth IRAs must fully distribute the account within 10 years, although certain eligible designated beneficiaries may qualify for different treatment. Even so, inherited Roth IRAs can still offer meaningful flexibility because distributions are generally tax-free if the rules are met. In many cases, that gives beneficiaries more control over the timing of withdrawals than they would have with an inherited traditional IRA, and it may allow additional time for tax-free growth depending on the beneficiary’s situation.

The Real Point

For the right household, a Roth conversion can be more than a tax move.

It can be a way to create options before they become scarce or too costly.

It can be a way to smooth your tax burden over time, rather than letting it build quietly in the background. It can be a way of planning in times of peace rather than in times of grief. And in some cases, it can help not just the surviving spouse, but the children who may one day inherit what remains.

That is why I believe Roth conversion planning is worth thoughtful analysis well before a crisis forces the issue.

Not because every conversion is smart.

Not because paying taxes now is fun.

Rather, because sometimes paying some tax now improves the overall shape of the long-term plan.

Closing Thoughts

If you are approaching retirement, already retired, or thinking more seriously about how widowhood, RMDs, Medicare premiums, healthcare costs, and legacy goals could affect your future, this is a good area to review carefully.

A Roth conversion may help. It may not.

What matters is understanding the trade-offs clearly and making the decision in the context of your full retirement income, tax, healthcare, and legacy plan.

The strongest next move is not guessing. It is looking carefully at the numbers while you still have choices. If you are wondering whether a Roth conversion before retirement could improve your long-term flexibility, schedule a call. We can help you evaluate trade-offs in the context of your overall financial plan.

Related Reading:

- How Roth Conversions Can Help You, Your Surviving Spouse, and Your Heirs.

- Financial Steps for Recent Widows: What to Do Now—and What Can Wait.

- Identifying and Overcoming 6 Key Threats to a Woman’s Retirement.

- The Social Security Tax Torpedo – Could It Happen to You?

- What the New 2025 Tax Law Means for You.

FAQs:

1. What is a Roth conversion?

A Roth conversion moves money from a traditional IRA or other pre-tax retirement account into a Roth IRA, with tax paid on the converted amount now in exchange for more future flexibility.

2. When should you consider a Roth conversion before retirement?

Often, the best time to evaluate it is in the years after work income declines but before Social Security and required minimum distributions fill up your tax return.

3. How does widowhood affect Roth conversion planning?

A surviving spouse may keep similar income sources but file as a single taxpayer, which can compress tax brackets and reduce future flexibility.

4. Can Roth conversions affect Medicare premiums or ACA health insurance costs?

Yes. Higher income from a conversion can affect IRMAA for Medicare and can also reduce ACA premium tax credits for households using Marketplace coverage.

5. Do recent tax law changes affect Roth conversion decisions?

They can. Temporary deductions and changing deduction limits may alter how much room you have for a conversion in a given year, which is why you should perform the analysis under current law.

6. Can Roth conversions help heirs, too?

Potentially, yes. Lower pre-tax balances can reduce future tax pressure on heirs, though inherited-account distribution rules vary by beneficiary type and should not be oversimplified.

7. When might a Roth conversion not make sense?

A Roth conversion may not make sense if the upfront tax cost is too high, if it triggers other costs such as higher Medicare premiums or lower ACA premium assistance, if the money is likely to be spent soon, or if the long-term benefit does not clearly outweigh the short-term cost.

Our practice continues to grow through introductions from our clients and friends. Thank you for your trust.

If you would like to discuss financial topics, including navigating new beginnings, managing your investments, creating a life plan, or saving for retirement, please schedule a call or a Zoom virtual meeting. We will be in touch.

Follow us:

Facebook | LinkedIn | Instagram | YouTube | Substack

Please note: We post information about articles that can help you make better money-related decisions on Facebook, LinkedIn, Instagram, and YouTube. You can subscribe to have articles delivered to you via Substack.

![]()

For firm disclosures, see here: https://apprisewealth.com/disclosures/