When it comes to saving for retirement, women face headwinds that men don’t. It starts with how much they earn. Women are paid about 80 cents for every dollar that men make. Time spent raising children and/or caring for aging parents often means they have shorter working careers, too. Lower earnings lead to lower savings and lower Social Security benefits. Another factor compounds these issues. Women also tend to live longer than men.

These factors put women at greater risk of outliving their retirement savings. Fortunately, there are some things women can do to build a larger and more protected nest egg. Consider implementing the following tips to get started:

- Build an Emergency Fund

According to estimates, nearly 80% of Americans live paycheck-to-paycheck. When it comes to your financial security, establishing an emergency fund covering at least three-to-six months of expenses should be a top priority. Start by opening a savings account for this purpose. Then transfer money from your paycheck to your emergency fund until you have built a sufficient balance. Interest rates are low, but you should keep your emergency funds in a savings account. That keeps them safe and can leave you confident that the money will be there if you need it. If you have trouble controlling your spending, you should also limit your credit card usage.

- Adopt a Plan to Repay Debts

If you have a significant amount of debt, deciding where to start can be overwhelming. I will never forget how I felt when I realized how much the credit card debt I accumulated when I was putting myself through college was costing me. It was worth it in the end, but it hurt at the time. After I graduated, I realized how much I was paying in interest expense. I immediately devised a plan to repay it.

First, I listed the amount I owed on each card and the related interest rate. I prioritized paying off the highest-rate debt first. That meant I paid the minimum payment on my other cards and paid as much cash as I could on the card with the highest interest rate. Once I paid that card off, I attacked the card with the second-highest rate next. I continued this process in succession until all my debts were repaid.

The other advantage to this approach was that once the first card was repaid, I could use it to pay for everyday expenses I knew I could pay without incurring additional interest. I don’t like to pay in cash that often. This approach also allowed me to use credit cards responsibly for everyday expenses.

- Build a Budget

You should understand what you spend your money on. I bought a townhouse about a year before I met my wife. At first, I wasn’t sure if I could afford it. For about a month, I tracked every penny I spent. I then entered all my spending into a spreadsheet. That helped me understand how I could cut my expenses if money got tight. It also increased my confidence that I could afford the monthly mortgage I would have to pay. Now I track our family expenses using Quicken. You can also use Mint or a spreadsheet template if that works better for you. I don’t get as granular now as I did before I bought my townhouse, but I do have an understanding of what we spend our money on.

When budgeting, you can use the 50/30/20 rule as a starting point. That rule says to allocate 50% of your spending toward needs like rent or a mortgage and utilities. The next 30% can be spent on wants such as dining out, entertainment, or vacations. The remaining 20% should be directed towards financial goals. These include saving for retirement and paying down debt. One thing to keep in mind. If you don’t have the discipline to repay your credit card each month, consider using a debit card instead.

- Start Saving… Yesterday

I know that sounds a little extreme. But time in the market adds more value than timing the market. In other words, one of the keys to wealth is investing for as long as you can. Yes, you should pay down debt before you save, but there are some important exceptions. If your workplace retirement plan includes a company match, you should consider at least saving enough to get the match even if you have outstanding debts. Why? Consider this. Say your plan gives you a 3% match if you contribute 6% or more to your retirement account. In other words, saving 6% in your retirement account gives you an automatic 50% return through the company match. That’s too good a return to pass up.

Albert Einstein is credited with saying, “Compound interest is the eighth wonder of the world. He who understands it, earns it … he who doesn’t … pays it.” Contributing even small sums to your retirement account can add up over time. If your employer doesn’t offer a retirement plan, you can open a traditional IRA or a Roth IRA to start saving. In 2021, you can contribute up to $6,000 to an IRA, or $7,000 if you are more than 50. The contribution limits for 401k’s are larger – $19,500, or $26,000 if you are over 50. If you are self-employed and have a retirement account for self-employed individuals, you can contribute as much as $58,000 in 2021, or $64,500 if you are over 50.

- Protect Yourself, Your Assets, and Your Loved Ones

Don’t forget about insurance. If you rent, make sure you get renter’s insurance to protect your valuables. If you own your home, make sure your homeowner’s insurance limits are sufficient – consider a replacement cost policy, too. Make sure the limits on your car protect you in case of an accident. There are some expensive cars on the road. Medical costs can be high, too. That means you may need more coverage than you think. Add an umbrella policy on top to protect your assets. While you may never use it, an umbrella policy is a cost-effective way to secure additional protection. If you need coverage but don’t have it, you may regret it. When it comes to life insurance, you are usually better served by buying term insurance instead of whole life insurance. Whole life policies can include big commission payments to the agents that you pay for. It can take years until the value of your policy is more than what you pay for it.

- Be a Long-Term, Rather Than a Short-Term Investor

Most women have a lower risk tolerance than men. This leads to holding more cash and bond investments than their male counterparts. While these types of investments can play an important role in your portfolio, don’t invest without keeping your long-term future in mind. If you are not planning to retire for 10 to 20 years or more, try not to let recent market volatility concern you. At Apprise, we work with clients to understand their risk tolerance. We use this work, along with a financial plan, to recommend a mix of stocks, bonds, and cash that can help you achieve your financial goals and live your desired lifestyle in retirement.

No one has a perfect track record when it comes to timing the market. If you are investing, you are expressing an implicit belief that the market will move higher over time. If you hold cash waiting for the market to fall to a certain level before investing, that cash can sit in your account for years. Holding cash can be more detrimental to your retirement success than experiencing volatility within the account.

Holding assets for the short- rather than long-term is akin to speculating rather than investing. It also can increase costs. You will likely pay more in taxes. It leads to more frictional costs that occur when you buy and sell securities. It also equates to more decisions. That means you have to be right more often to be successful.

- Diversify Your Investments

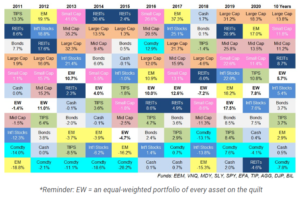

It can be easier to limit your investments to U.S.-based stocks and bonds. The tendency to invest based on where we live is often referred to as home-country bias. Over the last decade, a U.S.-centric investment approach has outperformed. But if we look at longer periods, the picture looks different. While history does not have to repeat, markets tend to be cyclical. What leads during one period often does not lead during the next.

As shown in the following chart, the best performing asset class changes from year-to-year.

Source: Updating My Favorite Performance Chart For 2020

Opportunities for future growth represent another factor supporting geographic diversification. Emerging markets, in particular, are forecast to have a better potential for GDP and population growth.

- If Applicable, Contribute to a Health Savings Account

I highlight the advantages of Health Savings Accounts, or HSAs, frequently on these pages. (For a detailed discussion of HSAs, check this blog.) If you enroll in a high-deductible health plan, you should open and contribute to an HSA. Why? HSAs represent the most tax-advantaged account you can open. They are triple tax-free. You get a tax deduction for your contributions. Funds invested in an HSA can grow tax-free. If you have unreimbursed qualified medical expenses at any time that you had a high-deductible health plan, you can withdraw funds from your HSA tax-free, too.

To qualify, your insurance coverage must have an annual deductible of $1,400 for individuals, or $2,800 for families. Annual contributions of up to $3,650 for individuals and $7,300 for families are allowed. Those who are 55 or over can contribute an additional $1,000. To optimize your HSA, treat it as a retirement account that you can invest in and fund any expenses you can without using your HSA.

- Consider Charitable Giving

Many individuals support local charities that are near and dear to them. You can maximize the benefit of your gifts by making them in a tax-efficient way. The 2017 Tax Cut and Jobs Act doubled the standard deduction. In 2021, it is $12,550 for single taxpayers and $25,100 for married couples. The larger standard deduction makes it harder to claim a tax benefit for your contributions. But there are still ways you can maximize the benefit.

- A married couple can deduct up to $600 of cash contributions in 2021 – $300 for singles.

- You can donate appreciated stock instead of cash.

- You can start a donor-advised fund.

- You can bunch your deductions and get a bigger overall tax benefit.

- If you are at least 70 ½, you can make a qualified charitable distribution (QCD) from your IRA.

If you are unsure of how any of the above techniques work, please give us a free call. We would be happy to review them with you.

CLOSING COMMENTS

The above represent some of the techniques women can use to build a larger and more protected nest egg. If you have questions about any of them or would like some help determining if they might be right for you, please schedule a free call. I would be happy to discuss them. You are also welcome to send me an email at philweiss@apprisewealth.com.

I’ll be back next week with “Apprise’s Five Favorite Reads of the Week.”

Have a great week.

Our practice continues to benefit from referrals from our clients and friends. Thank you for your trust and confidence.

We hope you find the above post valuable. If you would like to talk to us about financial topics including your investments, creating a financial plan, saving for college, or saving for retirement, please complete our contact form. We will be in touch. You can also schedule a call or a virtual meeting via Zoom.

Follow us: Twitter Facebook LinkedIn

Please note. We post information about articles we think can help you make better money-related decisions on LinkedIn, Facebook, and Twitter.

![]()

For firm disclosures, see here: https://apprisewealth.com/disclosures/