In this week’s Tuesday Tip video, Financial Planning for Women: How to Build a Strong Financial Foundation & Take Control of Your Future. Learn how to build a strong financial foundation and take control of your future with smart money moves.. Please watch the video below to learn more. If you would like a free review of your current financial situation, please use this link to schedule a free call. You can find an edited transcript below the video.

Life Transitions can be exciting—but they can also feel overwhelming, especially when it comes to finances. Whether you’re starting fresh after a divorce, adjusting to life on your own, or simply taking charge of your financial future, one thing is clear: A strong financial foundation gives you confidence and control. Today, I’ll walk you through the key steps every woman should take to build that foundation.

In this week’s Tuesday Tip, I would like to discuss Financial Planning for Women and review five steps you can take to help you build a Strong Financial Foundation.

Let’s take a look at why this matters

Too often, I’ve seen women hesitate to make financial decisions because they feel uncertain or unprepared. And I get it—you won’t find a financial playbook for life’s transitions. But I have some good news: You don’t need to have all the answers right away. What matters most is taking the right first steps. Let’s start with the basics.

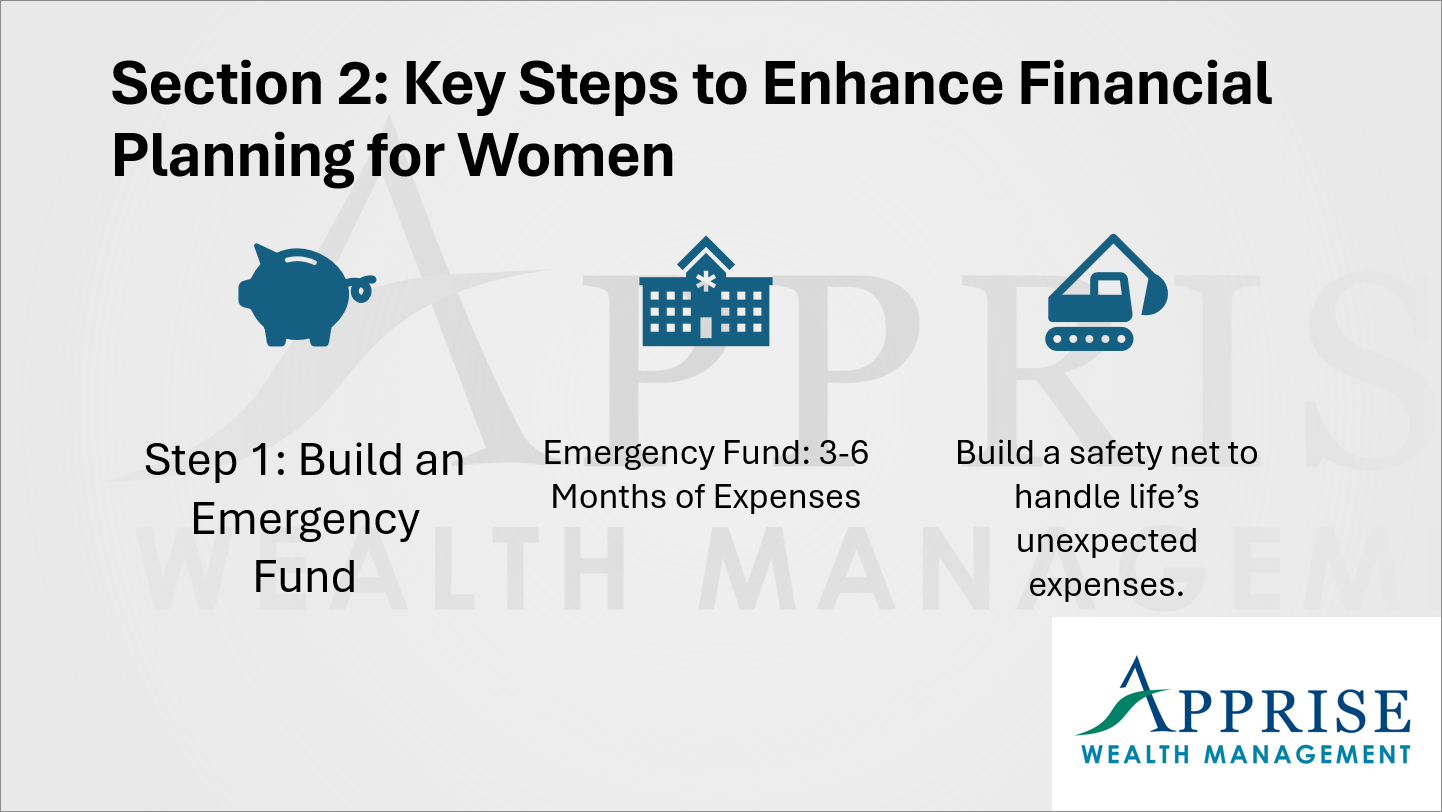

Key Steps to Enhance Financial Planning for Women.

Step 1: Build an Emergency Fund

First, an emergency fund is your safety net. Ideally, you want to have three-to-six months’ worth of living expenses set aside. Why? Because life happens. A job change, unexpected home or car repairs, or medical expenses can come out of nowhere. Having an emergency fund as a cushion means you don’t have to rely on credit cards or drain long-term savings to get through tough times.

If the idea of building up three to six months’ worth of living expenses sounds overwhelming, start small. Even setting aside $25 or $50 a week can add up over time. The goal is to turn saving into a habit.

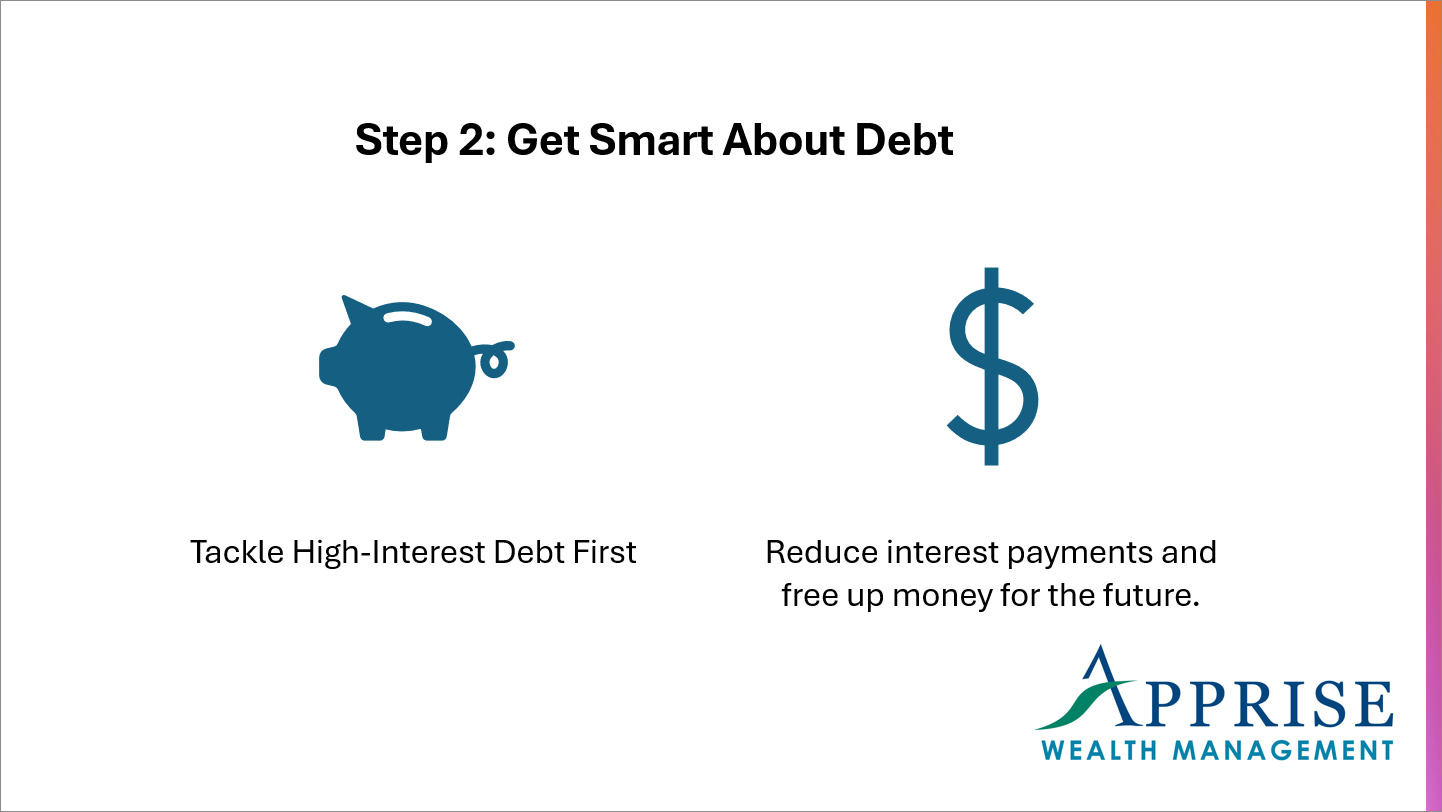

Step 2: Get Smart About Debt

Tackle High-Interest Debt First

Next, let’s talk about debt. If you have credit card debt or loans, focus on paying off the highest-interest debt first. The longer you carry a balance, the more you pay in interest—and that’s money that could be working for your future instead. Once you pay off your balance, as long as you pay in full each month, you won’t pay any interest in the future.

One strategy I like is the ‘debt avalanche’ method. List your debts, sort them by interest rate, and pay off the highest one first while making minimum payments on the others. Once that’s gone, move to the next. It’s efficient, and it saves you money in the long run. I followed this strategy when I had credit card debt after graduating from college. It worked great.

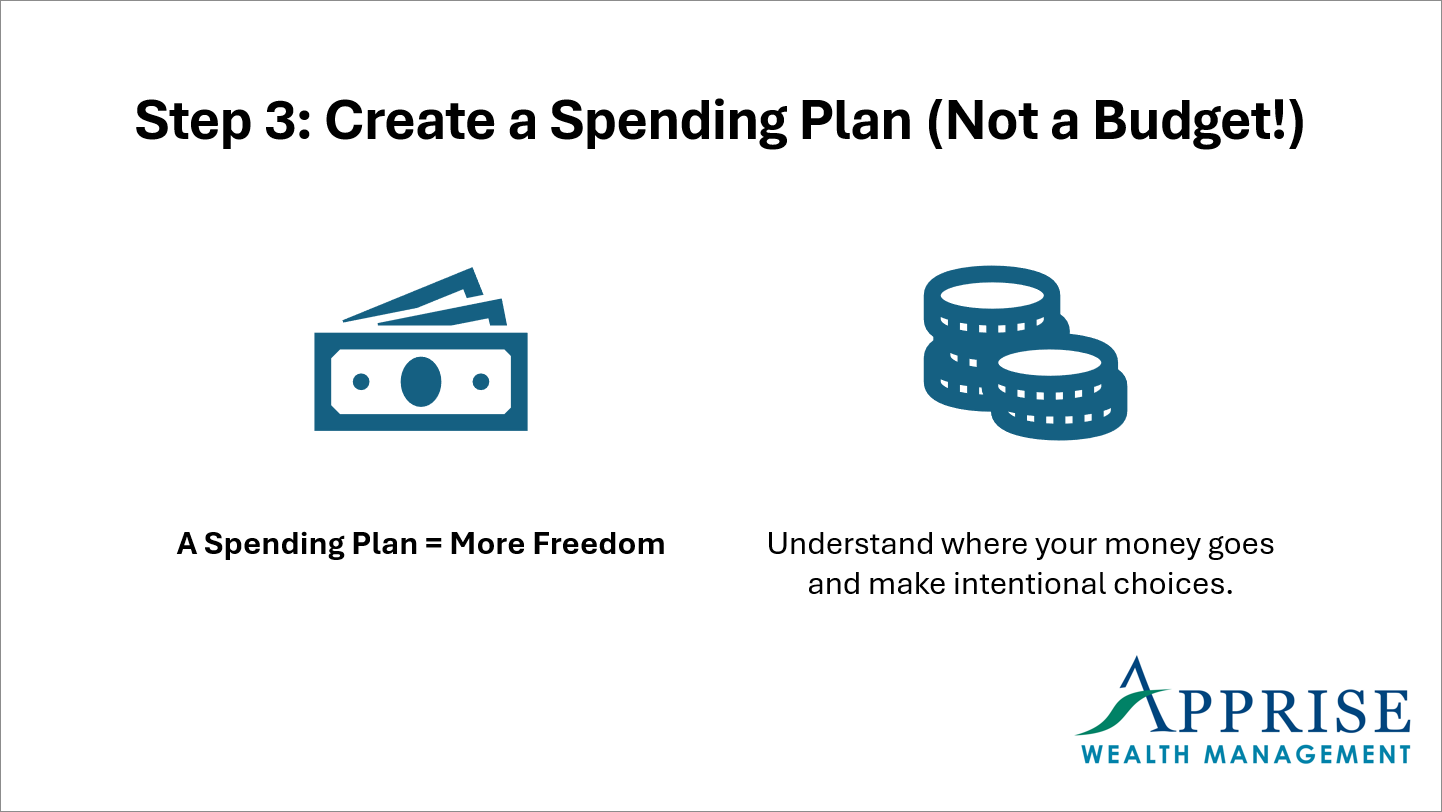

Step 3: Create a Spending Plan (Not a Budget!)

A Spending Plan = More Freedom

Now, I know the word “budget” makes some people cringe. So instead, call it a “spending plan.”Understandinghow much you take in and where your money is going each month allows you to better align your spending with what matters most to you.

Try this to start: Track your spending for a month. Then, use the 50/30/20 rule as a guide: 50% for needs like housing and groceries, 30% for wants like travel and entertainment, and 20% for savings and debt repayment. Once you see where your money goes, you may find it easier to start making more intentional choices.

Step 4: Start Saving for the Future—Now

Time in the Market Beats Timing the Market

One of the biggest financial myths is that you need a lot of money to start investing. Not true. The earlier you start—even if you can only put away a small amount—the better off you’ll be. Paying yourself first—depositing money directly in some type of savings or brokerage account rather than your checking account, makes it much easier to save, too.

If your employer offers a retirement plan, contribute enough to get the company match—it’s essentially free money. If you don’t have a workplace plan, open an IRA or a Roth IRA. Even small, consistent contributions grow over time thanks to compounding interest. As I always say, time in the market beats timing the market!

Step 5: Protect Yourself and Your Loved Ones

Insurance = Peace of Mind

Finally, don’t forget about protection. Having the right insurance—whether it’s health, life, disability, or long-term care insurance—can safeguard you and your loved ones from financial hardship. And estate planning matters, too. A simple will, updated beneficiaries, and powers of attorney can make sure your wishes are honored.

Building a strong financial foundation doesn’t require perfection—it’s about progress. Whether you’re starting from scratch or fine-tuning your plan, these steps can help you move forward with confidence.”

Take the First Step

“If you’re ready to take control of your financial future but aren’t sure where to start, let’s talk. Schedule a call with me, and we can start creating a plan that helps you move from uncertainty to clarity.

Remember, you don’t have to do this alone. I’m here to help. See you next time!

Our practice continues to benefit from referrals from our clients and friends. Thank you for your trust and confidence.

If you would like to speak with us about financial topics, including facing new beginnings, managing your investments, creating your life plan, or saving for retirement, please complete our contact form or schedule a call or a virtual meeting via Zoom. We will be in touch.

Follow us:

![]()

For firm disclosures, see here: https://apprisewealth.com/disclosures/